Cost Segregation

Commercial buildings are depreciated slowlyover 39 years. A cost segregation study carvesout components from buildings that qualify formore rapid depreciation, such as landimprovements and personal property.

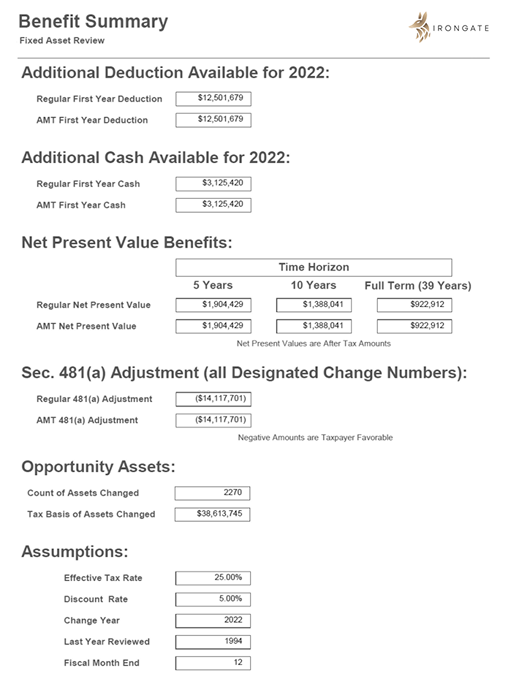

Individual

Asset Review

Individual assets are often inappropriately depreciated as part of a building, such asprocess-related plumbing, electrical, andventilation systems. This study identifies assetsqualifying for more rapid depreciation.

Capital to

Expense Studies

The new TPRs allow taxpayers to retroactively review expenditures that were capitalized butqualify as repair and maintenance expenses,such as replacing roof membranes, resealing parking lots, and replacing of HVAC components.

Retirement

Studies

Taxpayers often have ‘ghost assets’ in their fixedasset systems, such as removed roofs andHVAC components. A retirement study identifies these assets, allowing taxpayers to immediately deduct the remaining undepreciated basis.

Partial

Dispositions

The TPRs now allow taxpayers who makeimprovements to their facilities to immediately deduct the cost of the removed building components and to instantly write-off undepreciated basis amounts.

Bonus

Depreciation

Bonus depreciation allows taxpayers toimmediately write off from 30% to 100% of thepurchase price of a new asset, but is oftenmissed. This study identifies missed bonus opportunities.

Allows eligible developers to claim a tax credit of $500 to $5,000 for each newly constructed or substantially reconstructed qualifying residence,which includes single family homes, apartments, condominiums, and student housing.

§45L Energy Efficient Home Credit

Demolition

Costs

Demolition costs for building improvements are often capitalized with the cost of a new asset but can now be immediately deducted under the new TPRs.

Intangible

Asset Review

Taxpayers often have intangible assets on their fixed asset records that are amortized incorrectly or can be removed, such as an expired non-compete agreement. This study reviews intangibles for opportunities to accelerate amortization.

§179D Energy Efficient

Commercial Building

Deduction

Taxpayers who construct new buildings or make improvements to existing ones can take an immediate deduction of up to $5.65 per square foot for investments in efficient lighting systems, HVAC and hot water systems, and the building envelope.

.jpg)

.png)

.png)